Walk-Squawk Morning Wire

Macro Desk: Markets Are Trading the Promise of a Deal, Not the Reality

Markets came into this week heavily positioned for a positive outcome from the Trump-Xi summit. The narrative was simple: Trump arrived in Beijing with one of the largest U.S. business delegations in years, bringing executives from major technology, banking, aerospace, and agriculture companies, fueling speculation that China could eventually increase purchases of U.S. chips, energy, and agricultural products.

And to be fair, the headlines initially sounded constructive.

Trump called the relationship with China “better than ever before,” while Xi spoke about building stable long-term ties between the two countries. Discussions reportedly included expanded agricultural trade, energy purchases, tariff relief frameworks, and even potential investment cooperation between the two nations.

But underneath the optimism, the reality remains much murkier.

So far, there have been very few concrete details. No major confirmed soybean purchase package. No official breakthrough on semiconductor access. No finalized trade framework. Instead, what markets received was another extension of the negotiation process itself.

Trump later posted that he invited Xi to the White House in September, effectively extending the timeline for future talks and keeping markets focused on anticipation rather than resolution.

That raises an important question for markets:

Are we actually progressing toward meaningful agreements, or are investors simply getting pulled back into another cycle of “deal optimism” headlines?

The Contradiction Markets Are Ignoring

Right now, stocks continue behaving as if the geopolitical environment is steadily improving.

Tech remains resilient. Semiconductor stocks continue attracting aggressive dip-buying. AI-related names remain heavily crowded as traders continue betting that global AI spending and earnings growth will overpower macro risks.

But at the same time, the actual geopolitical backdrop remains highly unstable.

Xi delivered one of China’s strongest warnings yet regarding Taiwan, stating that mishandling the issue could lead to “collision or even clashes” between the two countries.

Meanwhile, the Iran conflict remains unresolved, with reports overnight that another commercial vessel was seized near the UAE as tensions surrounding the Strait of Hormuz continue.

That is the contradiction developing underneath this rally:

Markets are pricing diplomacy and stability, while the underlying geopolitical environment continues to signal fragility and unresolved conflict.

Why Grains Are Starting to Lose Momentum

Agriculture markets initially caught a bid into the summit on hopes China could step back into the U.S. grain market in a more meaningful way.

But overnight, soybeans and corn began pulling back as traders realized the summit has not yet produced any concrete purchase commitments.

That hesitation matters because the underlying fundamentals in China still do not point toward aggressive demand growth.

Chinese hog margins remain deeply pressured, and China’s own agricultural ministry recently projected softer soybean demand tied to a shrinking sow herd and weaker feed usage. Combined with already burdensome global soybean supplies, the market still lacks evidence that China urgently needs to dramatically expand purchases right now.

In other words, markets may have gotten ahead of themselves by pricing in a large agricultural trade package before actual details existed.

Could flash sales still appear? Absolutely. But until confirmed buying emerges, traders are left trading expectations rather than hard demand.

The Hidden Risk: The Market Is Becoming Too One-Sided Again

The stock market’s resilience continues to be driven largely by a narrow group of AI and semiconductor names.

That creates a dangerous setup where positioning itself becomes part of the rally.

As traders chase upside momentum in tech, dealers are forced to hedge by buying more stock, helping fuel what increasingly looks like a self-reinforcing gamma squeeze higher. The stronger the rally becomes, the more mechanical buying enters the market.

But these types of moves can create hidden fragility.

When markets become heavily concentrated in one narrative in this case AI, trade optimism, and soft-landing hopes it leaves very little room for disappointment.

And right now, several unresolved risks remain sitting underneath the surface:

No finalized U.S.-China trade agreements

Taiwan tensions continuing to escalate

Ongoing Iran/Hormuz disruptions

Oil prices remaining elevated

Inflation risks still pressuring bond markets

Extremely crowded AI positioning

The danger is not necessarily that the market collapses tomorrow. The danger is that markets are increasingly priced for positive outcomes before those outcomes actually materialize.

Why This Matters Going Forward

The next phase of this market likely depends on whether expectations finally turn into tangible policy actions.

If China follows through with meaningful agricultural purchases, semiconductor cooperation, or tariff reductions, markets can continue leaning into the global growth and AI narrative.

But if negotiations simply stretch out into another multi-month cycle of meetings, headlines, and vague promises while geopolitical tensions continue simmering underneath, the market may eventually begin questioning whether it got too optimistic too quickly.

For now, markets continue trading hope.

The question is how long investors remain willing to pay for anticipation without needing actual results.

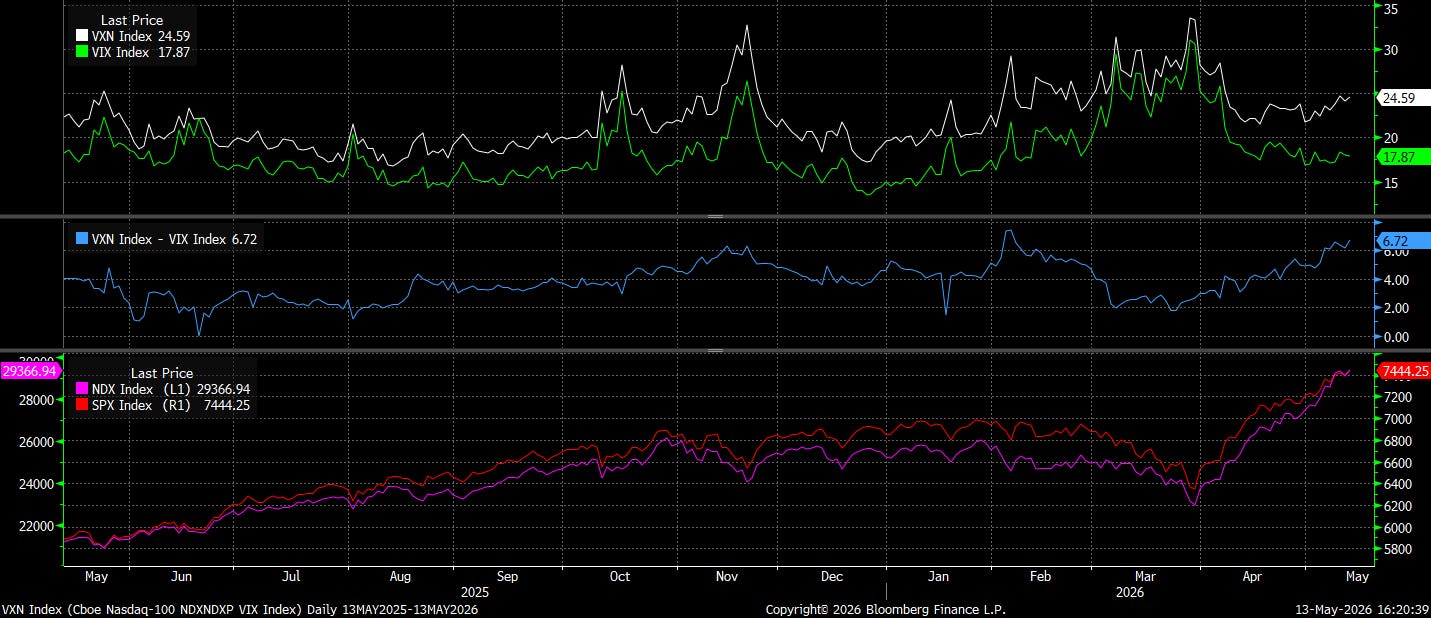

Nasdaq Volatility Is Quietly Warning About Fragile Market Leadership

One of the more interesting developments underneath this AI-driven rally continues to be the behavior of volatility markets.

While the Nasdaq continues pushing to new highs, Nasdaq volatility (VXN) remains unusually elevated relative to broader S&P 500 volatility (VIX). Normally during healthy, broad-based bull markets, volatility compresses across the board as investor confidence improves. But that has not fully happened here.

Instead, traders continue paying a premium for protection in tech and AI-related names even as indexes melt higher.

The reason likely comes down to concentration risk.

A small handful of mega-cap AI and semiconductor stocks continue driving a massive share of overall market performance. That creates a powerful momentum and gamma-driven melt-up higher, but it also leaves the broader market increasingly dependent on a narrow group of stocks continuing to perform flawlessly.

In simple terms, the market keeps moving higher, but the options market is quietly signaling that traders still do not fully trust the stability of the move underneath the surface.

That doesn’t automatically mean a major correction is imminent. In fact, persistent volatility premiums can remain elevated during strong momentum-driven rallies. But it does suggest the current market regime is becoming more fragile and increasingly dependent on continued AI leadership, aggressive dip-buying, and favorable macro headlines.

The rally continues, but traders are still paying for insurance.

Grain Desk

U.S. Cash Markets

Corn basis was mostly steady across the interior with processors and river locations showing only scattered adjustments. The Ohio River corn market firmed slightly, while Illinois River bids held mostly unchanged. Interior ethanol and processor demand remains supportive, especially with ethanol production rebounding sharply this week.

Soybean basis was mixed-to-firmer in select eastern Corn Belt locations, particularly Indiana processors and river terminals. Decatur, IL soybeans strengthened while Ohio River bean bids also improved. Western Corn Belt basis remains weak with large farmer movement and heavy nearby supplies still weighing on bids.

Key U.S. themes:

Ethanol grind jumped to 1.082 million bpd, up 65k bpd from last week, supportive for corn demand.

Ethanol stocks dropped sharply to 24.87 million barrels from 26.02 million last week.

Soymeal cash markets stayed firm with crushers well-owned into June and crush margins near $2.50-$3.30.

Corn futures continue finding support on ethanol demand and potential year-round E15 legislation debate in Washington.

South America Cash Markets

Brazilian soybean FOB values weakened again with July premiums reported around +20N to +25N and August premiums +35Q to +45Q. Farmer selling remains active as harvest pressure continues to cap rallies.

Brazil soymeal values were softer nearby, while Argentine soyoil basis strengthened following the sunflower crush plant fire in Argentina, which sparked concern about vegetable oil availability.

Corn:

Brazilian corn offers remain elevated with LH July around +109N offer.

Safrinha crop stress is still limited overall, though northern areas continue seeing moisture concerns.

Currency:

Brazilian real held mostly stable near 4.89/USD.

Argentine peso continues gradual weakness above 1,385/USD.

China & Global Demand

China remains cautious on nearby vegoil buying:

Traders noted China has shifted toward deferred purchases, especially December shipment windows, creating a near-term demand gap in palm oil and soyoil markets.

Weak nearby Chinese demand pressured Malaysian palm oil futures lower again overnight.

Dalian palm oil futures were lower while soyoil stayed mostly flat.

The market is also watching possible U.S.-China trade discussions closely, especially for any signs of renewed soybean or grain purchasing commitments.

Weather Rundown

U.S. Midwest

Weather overall remains favorable for planting and early crop development.

Key takeaways:

A mix of rain and sunshine over the next two weeks should support emergence and germination across much of the Corn Belt.

Some concern remains for drier areas from northeast Nebraska into Minnesota and eastern South Dakota where soil moisture is still marginal.

Frost risk continues across parts of Michigan and northern Ohio, though most analysts believe permanent damage risk remains limited due to early crop stages.

Broad Midwest rainfall coverage expands again late this week into next week with most areas expected to receive 0.30”-1.30” totals.

Temperature outlook:

Cooler eastern Midwest through Thursday.

Warmer western Plains and western Corn Belt with highs pushing into the 80s and low 90s by the weekend.

Delta & Southeast

Mostly favorable planting conditions continue with limited rainfall near term.

Some dryness is beginning to emerge from northern Florida into the Carolinas.

Markets are watching a potential rain event around May 18-21 closely.

Brazil

Brazil remains highly divided weather-wise:

Southern growing areas including Parana and Mato Grosso do Sul are expected to receive regular showers into late May, helping maintain favorable safrinha corn conditions.

Northern safrinha areas continue turning drier with crop stress slowly building.

Harvest and fieldwork progress remains strong in most other regions due to limited rainfall.

Argentina

Dry weather dominates most of Argentina over the next two weeks, allowing harvest to move quickly.

Only isolated light showers are expected in west-central and southeastern areas.

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates LLC and is, or is in the nature of, a solicitation. This material is not a research report prepared by R.J. O’Brien & Associates LLC. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien & Associates LLC believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

R. J. O’Brien & Associates, LLC (RJO) Disclaimer: This communication is not a research report prepared by R.J. O’Brien & Associates LLC’s (“RJO’s”) Research Department and should not be considered as such. It also does not provide information reasonably sufficient upon which to base a decision to enter into any derivatives business or transaction. This communication is instead part of a general marketing solicitation for you to consider doing derivatives business with RJO, but it is not an offer, a solicitation of an offer, or a recommendation for you to enter into any particular derivatives business or transaction with RJO or any other person. The risk of loss in trading futures and options on futures is substantial and each investor and trader must consider whether this is a suitable investment. You should not consider doing derivatives business with any person unless you understand the risks of derivatives and are capable (on your own or with the help of advisors you hire) of making your own independent trading decisions with respect to particular derivative transactions. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Information contained in this communication comes from sources that RJO believes are reliable, but we do not represent, warrant, or guarantee that such information is accurate or complete and it should not be relied upon as such.

Keep reading with a 7-day free trial

Subscribe to Walk-Squawk Market Talk to keep reading this post and get 7 days of free access to the full post archives.