Walk-Squawk Morning Wire

Macro Desk: Nvidia Faces Its Biggest Test Yet

After weeks of rising Treasury yields, escalating Middle East tensions, and signs of fatigue within the semiconductor trade, the market now turns its attention to the one company that has become synonymous with the AI boom: Nvidia.

The world’s most valuable company reports earnings after the close today, and while consensus expects another staggering quarter with revenue projected to grow roughly 80% from a year ago the bar has arguably never been higher. Nvidia has spent years conditioning investors to expect massive earnings beats and higher guidance. According to Bloomberg data, the company has averaged earnings surprises of roughly 15% and has consistently exceeded Wall Street expectations quarter after quarter. The question tonight isn’t whether Nvidia beats estimates. The question is whether it can once again exceed expectations that already seem impossible.

Options markets are currently pricing a move of approximately 5.5% in either direction following the report, which is remarkably close to Nvidia’s historical post-earnings reaction. In many ways, this earnings release has become a referendum not just on Nvidia, but on the entire AI investment cycle. Investors will be watching closely for signs that hyperscale spending remains robust, data center demand continues accelerating, and margins remain insulated from increasing competition.

The timing of the report is particularly important. The semiconductor rally has stalled in recent weeks as investors grapple with a changing macro environment. Long-term Treasury yields have surged to levels not seen since before the financial crisis, oil prices remain highly sensitive to developments surrounding Iran, and inflation concerns have resurfaced. Markets found some relief overnight as bond yields eased modestly and crude oil retreated, allowing equity futures to stabilize ahead of the report. Yet the broader concern remains that the AI trade has become increasingly crowded just as macroeconomic headwinds begin strengthening.

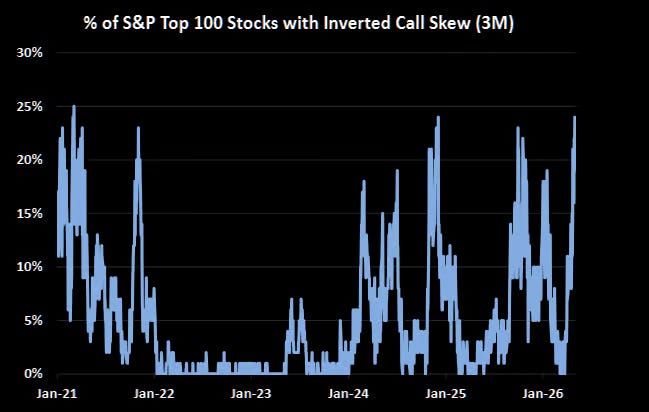

Perhaps the most underappreciated risk is positioning itself. Beneath the calm surface suggested by the VIX, investors have become heavily concentrated in a small group of MegaCap AI stocks. Call option activity remains elevated while downside hedging has steadily disappeared. Investors continue paying for upside participation rather than protection, reflecting a market more concerned with missing the next leg higher than preparing for potential downside risk.

This dynamic has created what many strategists describe as a fragile melt-up. As long as prices continue rising, momentum attracts additional buyers, leveraged products add exposure, and systematic flows reinforce the trend. However, should confidence begin to crack, those same flows could reverse quickly. It is this concentration and positioning not necessarily Nvidia’s fundamentals that may represent the greatest vulnerability in today’s market.

For now, though, Nvidia remains the market’s north star. A strong beat-and-raise quarter could easily reignite enthusiasm across semiconductors, AI infrastructure plays, and broader equity markets. Anything less than exceptional may force investors to confront a reality they have largely ignored for months: rising yields, elevated oil prices, and growing macroeconomic uncertainty.

In other words, tonight’s report isn’t simply about Nvidia’s earnings. It is about whether the AI narrative remains powerful enough to keep overpowering everything else. As goes Nvidia, so may go the market.

Grain Desk: Cash Markets & Weather Rundown

U.S. Cash Markets

Cash grain markets remain generally firm across key river locations and Eastern Corn Belt processors, while basis levels across portions of Iowa and Nebraska remain pressured by comfortable supplies and limited export urgency.

Corn

Corn basis was mostly steady to slightly firmer Tuesday.

Notable moves included:

Marion, Ohio strengthened another 2 cents to +35N for nearby delivery.

Ohio River bids improved 1 cent to +16N May and +24N July.

Nebraska processors firmed bids 2-5 cents at Ravenna, Minden and Blair.

Illinois River remained steady at roughly -10N nearby and -2N July.

Cedar Rapids held at -17N while Clinton remained -12N.

Export demand remains supportive:

June CIF Corn: 84N

July CIF Corn: 86N

Gulf premiums remain historically strong near $1.00 over futures, reflecting continued export competitiveness.

Processors remain well covered with many ethanol plants reportedly owning 45 days or more of corn grind. Cash ethanol margins continue near 40-47 cents per gallon, supporting steady processor demand.

Soybeans

Soybean basis remains mixed but generally steady.

Strongest locations include:

Decatur, Illinois: +25N nearby

Frankfort, Indiana: +20N June/July

Ohio River: +17N June, +20N July

Cairo export market: +40N July

Meanwhile western Corn Belt processors remain weak:

Cedar Rapids: -30N

Eagle Grove: -55N June

Mason City: -60N

Sheldon: -70N

Soymeal basis remained largely unchanged:

Central Iowa: -24N

Central Minnesota: -29N

Central Illinois: +18N

Cash crush margins remain near $3.00 per bushel, continuing to support domestic processor demand.

South America

Brazil

Brazilian soybean values improved modestly Tuesday.

Reported trade included:

July soybeans traded near +20N

August traded around +44Q

September bids reached +65U to +88U

Paranaguá basis strengthened:

July basis up 12 cents

August basis up 5 cents

Brazilian soymeal remained weaker:

June meal down $7

July down $5

August down $1

Crop conditions remain excellent despite a slight decline:

Paraná corn rated 93% Good/Excellent

Safrinha corn rated 82% Good/Excellent

While both slipped modestly from last week, conditions remain far above historical averages and well above last year’s levels.

Argentina

Argentina soybean crush for April reached 3.479 million metric tons, near trade expectations and running 1.2% ahead of last year’s pace for the season. Crush activity is expected to increase further during May.

Farmer selling remains relatively measured, with little urgency to move inventories amid stable currency conditions and favorable harvest weather.

China

China remains the wildcard demand story.

Treasury Secretary Scott Bessent indicated he will meet China’s Vice Premier ahead of President Xi’s September visit to discuss trade agreement details. However, he also stated the U.S. is not in a hurry to extend the current trade truce beyond November.

Key developments:

China has still not purchased U.S. new-crop soybeans.

Old-crop soybean purchases appear unlikely.

Traders continue watching for any reduction in China’s current 10% tariff on U.S. agricultural products as a first step toward renewed buying.

The market continues to speculate that eventual Chinese purchases could include:

Soybeans

Corn

Sorghum

Soft wheat

Export inquiries for SRW wheat have reportedly increased, supporting wheat futures despite managed money remaining net short.

Crop Progress Recap

Planting progress remains one of the least threatening stories for the grain market.

Across much of the Corn Belt:

Corn planting is essentially wrapping up.

Soybean planting continues at a historically rapid pace.

Emergence has generally been favorable.

Soil moisture has improved substantially across many previously dry regions.

The market’s primary focus has shifted from planting delays to weather-driven yield potential.

Weather Rundown

Midwest

The forecast remains broadly favorable for crop development but increasingly challenging for fieldwork.

Key themes:

Multiple rounds of rainfall over the next 7-10 days.

Best coverage from eastern Nebraska through Iowa, Minnesota, Wisconsin, Illinois, Indiana and Ohio.

Most areas receive 0.50-2.00 inches.

Localized totals could exceed 3 inches.

The moisture is particularly beneficial for:

Eastern Nebraska

Central and northern Iowa

Southern Minnesota

Eastern South Dakota

where soil moisture deficits still linger.

Frost Risk

A fresh frost threat develops Tuesday night into Wednesday morning.

Areas at risk include:

Eastern North Dakota

South Dakota

Northeastern Nebraska

Western and central Minnesota

Most corn and soybean acres have not yet emerged, limiting widespread damage potential. However, emerged crops could experience leaf burn and localized stand damage.

Delta

The Delta turns significantly wetter.

Heavy rainfall is expected from:

Mississippi

Alabama

Western Georgia

through next week.

Localized flooding and planting delays are possible, particularly in the lower Delta.

Brazil

Weather remains largely favorable for safrinha corn.

Paraná and southern Brazil remain wet.

Soil moisture remains excellent.

Fieldwork delays continue in some areas.

Northern Brazil remains the primary concern as crop stress slowly increases where recent rainfall has missed production areas.

Argentina

Dry weather dominates the forecast for the next two weeks, allowing harvest activity to progress rapidly with very few interruptions.

Bottom Line

Cash markets remain firm in export channels and portions of the Eastern Corn Belt, while Brazil continues to enjoy excellent safrinha crop conditions despite minor deterioration. China remains largely absent from U.S. soybean markets but trade negotiations continue to be closely monitored. Weather remains mostly favorable for crop development, with beneficial rains across much of the Corn Belt offset by localized frost concerns in the Northern Plains and increasing wetness that could slow the final stages of planting.

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates LLC and is, or is in the nature of, a solicitation. This material is not a research report prepared by R.J. O’Brien & Associates LLC. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien & Associates LLC believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

R. J. O’Brien & Associates, LLC (RJO) Disclaimer: This communication is not a research report prepared by R.J. O’Brien & Associates LLC’s (“RJO’s”) Research Department and should not be considered as such. It also does not provide information reasonably sufficient upon which to base a decision to enter into any derivatives business or transaction. This communication is instead part of a general marketing solicitation for you to consider doing derivatives business with RJO, but it is not an offer, a solicitation of an offer, or a recommendation for you to enter into any particular derivatives business or transaction with RJO or any other person. The risk of loss in trading futures and options on futures is substantial and each investor and trader must consider whether this is a suitable investment. You should not consider doing derivatives business with any person unless you understand the risks of derivatives and are capable (on your own or with the help of advisors you hire) of making your own independent trading decisions with respect to particular derivative transactions. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Information contained in this communication comes from sources that RJO believes are reliable, but we do not represent, warrant, or guarantee that such information is accurate or complete and it should not be relied upon as such.

Keep reading with a 7-day free trial

Subscribe to Walk-Squawk Market Talk to keep reading this post and get 7 days of free access to the full post archives.