Walk-Squawk Morning Wire

Ceasefire Sparks Relief But Markets Want Proof

Markets are sharply higher this morning following a surprise de-escalation overnight, as the U.S. and Iran agreed to a two-week ceasefire, with Tehran signaling it will move toward reopening the Strait of Hormuz.

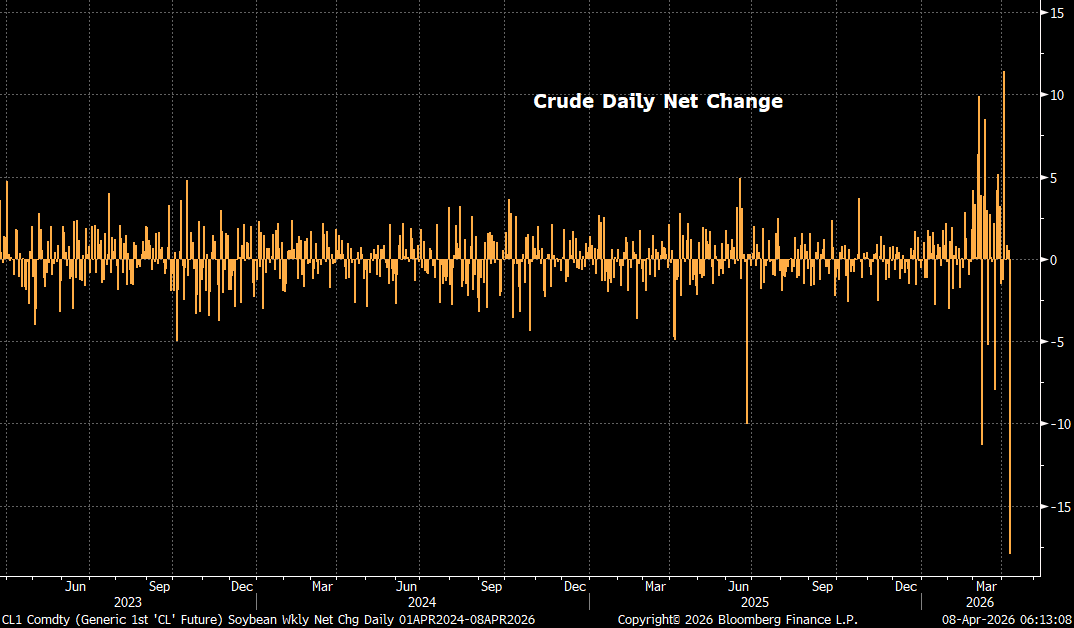

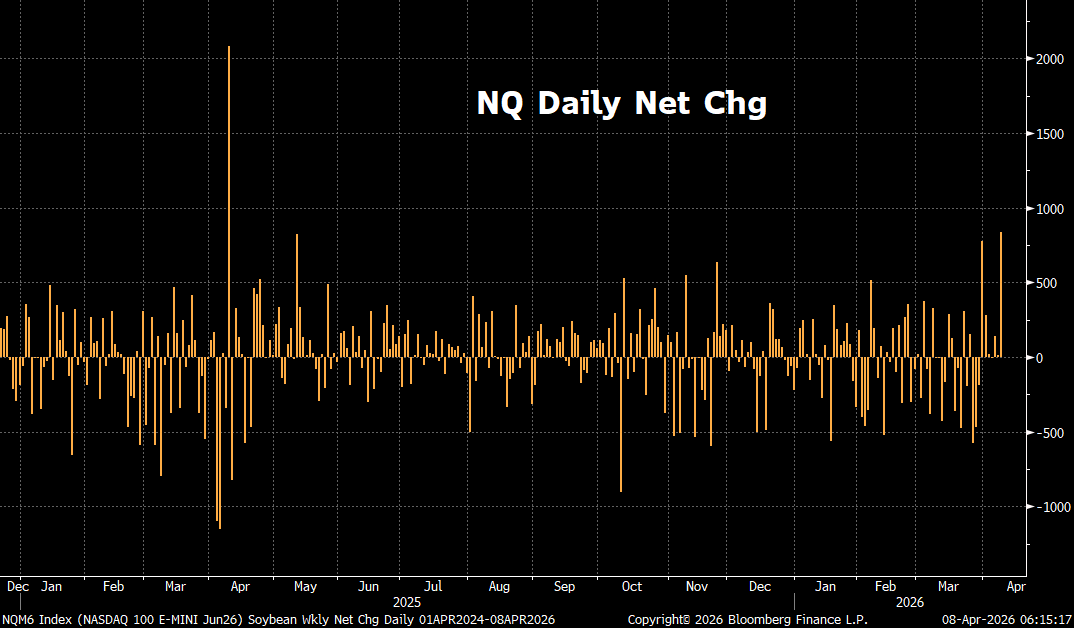

The reaction has been immediate. Nasdaq futures are up over 3%, S&P futures pushing close to 3%, while crude oil has collapsed more than $18 a rapid unwind of the geopolitical risk premium built over recent weeks.

This is a classic relief rally, driven by short covering and the removal of worst-case energy disruption scenarios.

But the underlying situation remains fluid.

Despite the ceasefire, hostilities have not fully stopped, with reports of continued attacks across the region, including drone interceptions in Kuwait, missile threats in the UAE, and strikes tied to both sides. Iran also confirmed a hit to its Lavan refinery, reinforcing how fragile conditions remain.

Vice President JD Vance described the truce as “fragile,” while confirming U.S. military objectives have been achieved. Talks are expected to continue later this week, with Pakistan set to host negotiations but key details around timing, enforcement, and scope remain unclear.

Energy Is Still the Story

The focus now shifts to whether the ceasefire translates into actual flows.

The Strait of Hormuz has been effectively constrained for weeks, leaving more than 800 vessels stranded in the Persian Gulf many loaded with crude, refined products, and LNG. A reopening could ease global supply pressures but so far, movement remains limited.

Iran has signaled conditional passage, while the U.S. has framed it as a full reopening. Whether ships move freely, face tolls, or remain restricted is still unresolved.

For now, shipowners are cautious. After weeks of disruption and security risks, traffic won’t normalize overnight even under a ceasefire.

There is also a growing view that Iran may continue to use Hormuz as leverage, allowing selective flows while maintaining pressure on global energy markets.

Cross-Asset Impact

The collapse in crude is already feeding through to ag markets:

Bean oil sharply lower as biofuel demand expectations reset

Corn and wheat softer

Soybeans relatively stable

Bottom Line

Markets have been given a window to breathe.

But this is a pause, not a resolution.

If Hormuz reopens meaningfully, the risk premium continues to unwind.

If not, or if the ceasefire breaks, volatility returns quickly.

For now, markets are trading relief

but waiting for confirmation in the flow of oil.

Relief Rally vs. Reality Check

Markets are reacting exactly how you’d expect — sharply, but not evenly.

Crude is the headline. A $15–$18 drop is a pure unwind of geopolitical risk premium tied to the Strait of Hormuz. This wasn’t new supply — it was crowded positioning getting flushed.

Equities are a different story.

Nasdaq is up ~850 points strong, but not extreme. Compared to prior events like “Liberation Day,” where we saw multiple 1k point downside days, the lead-up this time was far more controlled. Pullbacks were mostly in the 300–500 point range.

That matters.

It suggests the market never fully priced in a worst-case scenario. So when the ceasefire hit, the reaction was more measured.

Call it a mini Liberation Day a relief move driven by short covering, not a full reset higher.

Lower oil helps the macro backdrop, but this rally is still fragile. The ceasefire is uncertain, and markets remain highly sensitive to headlines.

Ag Cash, Global Flow, and Weather Setting the Tone

U.S. Cash Markets

Cash continues to quietly firm underneath a weaker futures tone.

Interior corn basis is steady to stronger, with processors still bidding for nearby needs as farmer selling remains limited. Ethanol plants are largely covered into summer, but spot demand is still showing up where logistics are tight.

Soybean basis is mixed but improving at processors, with crushers maintaining solid margins near $2.50. The farmer remains mostly out of the market, which is keeping nearby supply tight despite futures pressure.

Freight remains elevated but stable, and CIF bids are still firm telling you export demand hasn’t disappeared, just not chasing.

South America

Brazil remains the anchor and still looks good.

Safrinha corn 100% planted with strong conditions (~93% good/excellent)

Soybean harvest essentially complete (~96%)

Weather = mostly favorable with good moisture coverage

That said:

Northern Brazil showing some drier risk in the 6–10 day

Argentina dealing with excess rain + flooding, slowing fieldwork and raising localized quality concerns

Big picture:

Supply is there but it’s not perfect, and the market is watching weather closely.

China

China remains a quiet but bearish undertone.

Weekly crush came in below expectations (1.625 MMT)

Hog margins are deeply negative (~-$34/head) → demand headwind

Large soybean stocks + slowing meal trade

At the same time:

China is actively looking to reduce soybean usage in feed rations

Margins favor Brazil over U.S. beans near-term

Translation:

China is not a demand driver right now more of a drag.

Weather Rundown

U.S.

Midwest: Wet soils + recent rains = early planting delays

More rain coming (1–3”) → keeps pressure on near-term progress

Delta/Southeast: Warmer + drier → good planting conditions

South America

Brazil: Good mix of rain/sun → overall supportive

Argentina: Too wet → flooding + delays, but not widespread damage

Bottom Line

U.S. cash = firm underneath weak futures

South America = large supply, but weather still matters

China = demand headwind

Weather = short-term pressure, longer-term uncertainty

This is a market where:

Cash is holding better than futures but demand isn’t chasing yet.

Until that changes, rallies likely need help from weather or macro, not just flows.

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates LLC and is, or is in the nature of, a solicitation. This material is not a research report prepared by R.J. O’Brien & Associates LLC. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien & Associates LLC believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

R. J. O’Brien & Associates, LLC (RJO) Disclaimer: This communication is not a research report prepared by R.J. O’Brien & Associates LLC’s (“RJO’s”) Research Department and should not be considered as such. It also does not provide information reasonably sufficient upon which to base a decision to enter into any derivatives business or transaction. This communication is instead part of a general marketing solicitation for you to consider doing derivatives business with RJO, but it is not an offer, a solicitation of an offer, or a recommendation for you to enter into any particular derivatives business or transaction with RJO or any other person. The risk of loss in trading futures and options on futures is substantial and each investor and trader must consider whether this is a suitable investment. You should not consider doing derivatives business with any person unless you understand the risks of derivatives and are capable (on your own or with the help of advisors you hire) of making your own independent trading decisions with respect to particular derivative transactions. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Information contained in this communication comes from sources that RJO believes are reliable, but we do not represent, warrant, or guarantee that such information is accurate or complete and it should not be relied upon as such.

Keep reading with a 7-day free trial

Subscribe to Walk-Squawk Market Talk to keep reading this post and get 7 days of free access to the full post archives.